Many planning for financial security want to understand and implement robust measures to protect their family and finances. One such crucial instrument that everyone should know about is term insurance. Term insurance stands out as a cornerstone of financial planning, offering a safety net to one’s family against life’s uncertainties. It is a cost-effective form of life insurance, wherein term insurance will provide financial security to the beneficiaries in case of the death of the insured person during the policy term. This article delves into the concept, types, importance, and real-world examples of term insurance, highlighting why it should be an integral part of one’s financial planning. For anyone who values financial security and peace of mind, term insurance is indispensable.

What is Term Insurance?

Term insurance is a life insurance product that offers coverage for a specified period, known as the policy term. In the unfortunate event of the policyholder’s death during this term, the insurance company pays the predetermined sum assured to the nominee. Unlike other life insurance products, term insurance is characterized by its affordability and the absence of maturity benefits, making it a pure risk cover.

Key Features of Term Insurance

Term insurance is a simple and essential financial tool that provides life cover to secure your family’s future. It offers peace of mind by ensuring financial stability for your loved ones in your absence. With affordable premiums and straightforward benefits, it’s a practical choice for protecting your family.

- Provides financial security to dependents in the absence of the policyholder: It gives your family the money they need to cover their daily expenses and maintain their lifestyle. This support helps dependents handle major life costs like education, healthcare, or rent when they are not around. It reduces the financial burden on loved ones during tough times.

- Does not include a savings or investment component: This insurance policy is designed only to provide life coverage and does not build wealth over time. It focuses entirely on protecting your family without adding complex investment features. The simplicity makes it easy to understand and manage.

- Affordable premiums compared to other insurance products: The cost is lower than other insurance types, making it a practical choice for families with limited budgets. It allows you to secure a high coverage amount without straining your finances. This affordability makes it accessible to many individuals seeking essential life protection.

Types of Term Insurance

Term insurance comes in various types, catering to diverse financial needs and goals. From fixed coverage plans to those with growing or reducing benefits, each option offers unique advantages. Understanding these variations helps policyholders choose the best plan for their future security.

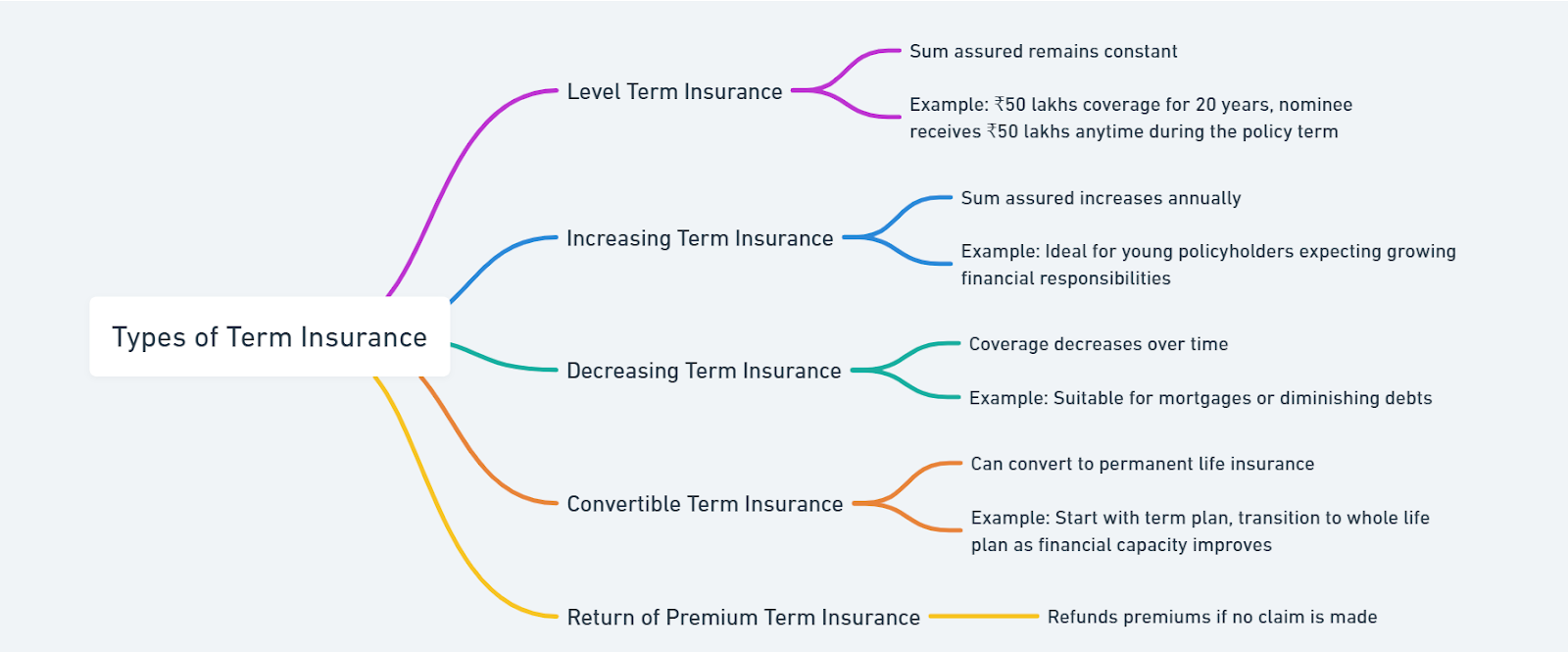

Level Term Insurance

- Consistency: The sum assured stays fixed throughout the policy, providing dependable financial security.

- Simplicity: Policyholders know exactly what their nominees will receive, ensuring peace of mind.

- Example: A person choosing ₹50 lakhs coverage for 20 years guarantees their family the same amount, regardless of when the claim happens.

Increasing Term Insurance

- Growth: The coverage grows every year, helping policyholders manage rising financial needs.

- Adaptability: Suitable for young professionals whose financial responsibilities, like education or family needs, will increase over time.

- Example: A young person starts with a smaller premium and gradually builds a larger safety net for their family.

Decreasing Term Insurance

- Alignment: Coverage reduces as liabilities, like home loans or car loans, are paid off over time.

- Cost-Effective: It focuses on protecting against specific debts, which helps lower premiums.

- Example: A homeowner can secure their mortgage, ensuring their family won’t face repayment burdens if something happens.

Convertible Term Insurance

- Flexibility: It allows policyholders to upgrade their plan to a permanent one as their financial situation improves.

- Future-Ready: Provides an option to adapt coverage for long-term goals without needing a new policy.

- Example: A person starts with a term plan and later transitions to whole life insurance to ensure lifelong coverage.

Return of Premium Term Insurance

- Savings: Refunds the entire premium amount if the policyholder outlives the term, offering risk coverage and financial returns.

- Dual Benefit: Combines insurance protection with a form of savings, making it an appealing option.

- Example: Someone pays premiums for 20 years and receives the total amount back if no claim is made during that period.

Importance of Term Insurance

Term insurance offers more than just life coverage; it provides essential benefits that cater to various financial needs. From ensuring family security to offering tax savings and customizable options, it is a practical solution for comprehensive protection. Understanding these benefits helps make an informed decision.

- Financial Security for Family: It provides a safety net for loved ones, ensuring they can maintain their standard of living even in the absence of the policyholder. It covers essential needs like daily expenses, children’s education, and medical bills. This financial cushion offers peace of mind during difficult times.

- Cost-Effectiveness: It allows individuals to secure significant coverage without straining their finances. The premiums are affordable compared to other insurance types, making it accessible to a broader audience. It is a smart choice for anyone looking to balance cost and protection.

- Debt Protection: This policy ensures that outstanding loans like home loans, personal loans, or credit card debts are fully cleared. It prevents the family from bearing any financial burdens caused by unpaid liabilities. This benefit protects assets like a house or car from being sold to repay debts.

- Tax Benefits: Policyholders can save on taxes while ensuring financial security for their families. Premium payments qualify for deductions under Section 80C, reducing taxable income. Additionally, death benefits received by the nominee are entirely tax-free, offering a double advantage.

- Customizable Options: Riders like critical illness cover or accidental death benefits provide additional layers of protection. These features can be tailored to suit individual needs, enhancing the policy’s overall value. For example, a waiver of premium ensures the policy remains active even if the policyholder cannot pay due to unforeseen circumstances.

Term Insurance FAQs

Explain the term insurance and its purpose.

Term insurance is a life insurance policy offering coverage for a fixed period. Its purpose is to provide financial security to beneficiaries if the insured passes away during the policy term.

What is term insurance, and how does it work?

Term insurance is pure life cover. If the policyholder dies during the policy term, the sum assured is paid to the nominee. If the policyholder survives, no payout is made unless it’s a return-of-premium plan.

Can you provide term insurance examples?

Level Term Plan: ₹1 crore coverage for 30 years at ₹10,000 annual premium. Decreasing Term Plan: Coverage reduces with loan repayment milestones.

What happens if I outlive my term insurance?

Traditional term plans provide no benefits if you outlive the policy. However, in return of premium plans, all premiums paid are refunded.

Why choose term insurance over other life insurance plans?

Term insurance is affordable and provides high coverage, making it ideal for individuals seeking pure-risk coverage without investment or savings components.