Financial institutions are the backbones of the modern economy. They act as intermediaries between saving and borrowing, hence playing a significant role in determining the flow of funds. Economic activities such as lending, accepting deposits, and investment are conducted by financial institutions. Financial institution’s examples include diversified needs such as saving, lending, and internet banking in the commercial banks: SBI, and HDFC, among others. Other examples are the NBFCs: Bajaj Finance and its microfinance and consumer loan products, Insurance companies – LIC, ICICI Lombard among others, investment solutions- mutual funds: SBI Mutual Fund. Together, all these institutions ensure the efficient distribution of funds and economic stability.

What is a Financial Institution (FI)?

Financial institutions are firms that provide financial services to individuals, businesses, and governments. These institutions promote economic activities through credit extension, protection of deposits, and fund management.

Financial institutions are institutions that handle money and other forms of financial wealth. They are guardians of public funds and also providers of loan services, investment services, and means of effecting payments. Their ultimate goal is to have liquidity in the economy, businesses thrive, and capital be put to its right use.

Attributes of Financial Institutions

Attributes of financial institutions define their role in supporting economic activities. Key attributes include trust, regulation, liquidity management, and diverse service offerings.

- Intermediate Function: Financial institutions act as an intermediary between savers and borrowers.

- Regulation: They are regulated by the government and the central banks for safety.

- Diversification: They provide all types of financial products, savings, and investments.

How Do Banks Make Money?

The bank in a financial setup is very essential source of income in the financial business process of a firm. Sources of the Bank’s income include Interest margin.It is the highest source of income for banks as it depends on the gap between the loan interest charged on a loan and the interest paid on a deposit. Another source is fees and investments.

- Interest Income: Banks lend money to individuals and other businesses at a rate higher than what they collect through saving accounts. For example, they collect 10% in loans but pay only 3% on deposits.

- Service Charges: Banks charge for keeping accounts, doing transfers, and using the ATM. The more they collect, the higher their service income.

- Investments: Banks invest in government bonds, bonds, and other securities to earn money.

- Foreign Exchange Services: Revenue is derived from foreign exchange and other foreign operations

- Revenue Derivation: A bank earns revenue on advances to new ventures.Revenue from service charges on Internet banking.

Are All Financial Institutions Safe?

Safety is very sensitive to the customers who put their savings in them invest in them or borrow money from them. Factors that Influence Safety. Not all financial institutions are secure. Their safety depends on the regulatory and operational effectiveness of a financial institution with market conditions. For instance, banks are heavily regulated compared to NBFCs. In this manner, the risk for depositors is reduced.

How to Check the Safety of Financial Institutions?

- Regulation: Check if the institution is registered with the central bank.

- Reputation: Search for ratings and reviews by customers.

- Insurance Coverage: Find out which institutions have coverage under deposit insurance schemes.

Examples of Safe and Risky Institutions

- Safe: Public sector banks like State Bank of India.

- Risk: Unregulated lending apps.

Measures Adopted to Make Safer: Governments have brought stringent rules and ensured the coverage of deposit insurance. The customers must choose the banks according to the set norms.

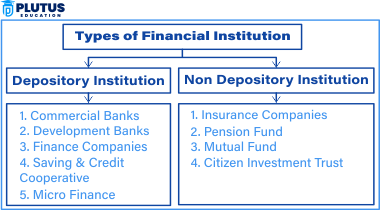

Types of Financial Institutions in India

In addition, the Indian financial system involves a group of institutions that address a variety of financial needs, thereby greatly aiding in the nation’s economic growth. Such institutions include banks, NBFCs, insurance companies, and mutual funds, which fulfill the various requirements of the country. The classification of financial institutions is as follows:-

Banking Financial Institutions

Banks are an important part of the financial infrastructure in India. They mobilize public savings and provide credit along with other financial services.

- Examples: Punjab National Bank (PNB) and ICICI Bank are the largest commercial banks in India.

- Services: They provide savings accounts, recurring and fixed deposits, personal and business loans, and trade financing. For example, PNB has loans for agriculture suited to rural India, and ICICI Bank has a digital banking and credit card business.

Non-Banking Financial Institutions (NBFCs)

NBFCs are financial services institutions that do not require a license from the banks. They usually operate in niche markets and target less-banked geographies.

- Examples: Bajaj Finance and LIC Housing Finance are two large NBFCs in India.

- Specializations: Bajaj Finance offers car and consumer finance. LIC Housing Finance offers home finance. A bank cannot take demand deposits. However, they are very active in microfinance and leasing.

Insurance Companies

Insurance companies in India help individuals and companies handle risks like loss of life, health-related problems, and general insurance coverage.

- Examples: Life Insurance Corporation is the largest player in the life insurance market, and it also claims the title for the health and general insurance sector.

- Importance: These companies safeguard financial security against unforeseen problems such as accidents, hospitalization, and loss of property.

Mutual Funds

Mutual funds allow aggregation of funds which experts then invest to yield returns. They have a combination of equities, bonds, and other securities in their portfolio.

- Examples: The two major players in this field are SBI Mutual Fund and HDFC Mutual Fund.

- Benefits: They have SIPs and diversification for individual investors.

Indian Financial Institutions Examples

The financial system in India is robust and diversified. Many institutions serve diverse economic and social needs. These enhance the country’s financial infrastructure. Such institutions provide crucial services in lending, savings, insurance, and investment, besides aiding in developing the economy and advancing financial inclusion and stability.

Indian Commercial Banks

Commercial banks are the pillar of India’s financial system. They accept deposits, and advance loans, and provide various financial services to different people, organizations, and governments. All these are the mainstays of India’s economic activities. Examples of Commercial Banks in India are:-

- State Bank of India (SBI): SBI is the largest public sector bank in India. It offers all financial services from personal loans, and agricultural finance to wealth management products. Rural outreach supports financial inclusion and infrastructure development in rural areas.

- HDFC Bank: HDFC Bank is one of the leading private sector banks that has clicked well on the digital banking front and in the delivery of customer-centric services as well. HDFC Bank offers personal and corporate loans, credit cards, and investments to the urban and semi-urban customer base.

- Punjab National Bank (PNB): Punjab National Bank is one of the public sector banks that offers diversified banking solutions to the nation. It contains export financing, corporate loans, and housing loans to nurture industrial growth in India.

- Axis Bank: The leading private sector bank exercises core competencies of retail banking, digital payments, and SME financing. The diversified range of credit products props up entrepreneurship.

- Bank of Baroda (BoB): This is a Global Public Sector Bank that addresses business needs by means of forex trading, global banking products, and various other international trades.

Non-Banking Financial Institutions in India

The NBFCs play the most crucial roles in the Indian economy. They run specialized financial service companies; therefore, they are able to reach the populations who remain under-served and focus areas such as rural and semi-urban fields. They neither hold a bank license nor specialize in lending services and investments. Examples of Non-Banking Financial Institutions are:-

- Bajaj Finance: It is an NBFC, mainly engaged in consumer durable loans, EMI financing, and personal credit. It also includes SME loans to fill the credit gap of small businesses.

- Muthoot Finance: The company specializes in gold loan services and offers quick and easy access to funds for individuals and small businesses requiring liquidity.

- HDFC Ltd.: HDFC Ltd. has specialized in housing finance, which has enabled millions of Indians to acquire affordable home loans

- Shriram Transport Finance: This is an NBFC that finances vehicles for commercial purposes besides personal use, thus supporting transportation industries.

- LIC Housing Finance: An NBFC subsidiary of LIC, it offers home loans, refinancing, as well as other services related to property, which makes housing more affordable.

Insurance Companies in India

Insurance companies protect a person and firm from risks against life, health, property, or other unforeseen events. An important part of the financial structure of India which provides financial protection. Examples of Insurance Companies are:-

- Life Insurance Corporation (LIC): It is a state-owned insurance company that offers life, retirement plans, and child education in India. Life Insurance Corporation happens to be one of the trusted insurance companies.

- ICICI Life: This is a health and general private insurer offering home insurance and corporate risk solutions, among other products.

- SBI Life Insurance: This is a subsidiary of SBI and offers relatively low-priced life insurance plans and pension schemes cateringtor middle-income people only.

- HDFC ERGO: It has emerged recently to be one of the very popular general insurance services. They offer motor, health, and travel insurance along with easy settlement of claims.

- Max Life Insurance: Deals specifically with long-term savings and protection plans involving wealth creation and then benefits that are secured at the time of retirement.

Mutual Funds in India

Mutual funds collect money from various investors to pool it together into investments of diversified portfolios handled by experts. They are apt for those interested in returns without handling either stocks or bonds directly. Examples of Mutual Funds are:-

- SBI Mutual Fund: It is one of the biggest fund houses in India. SBI offers SIPs and diversified investment products, apt for both risk-averse and risk-seeking investors.

- HDFC Asset Management Company (AMC): HDFC AMC offers equity, debt, and hybrid schemes that have stable returns and are well-managed

- ICICI Prudential Mutual Fund: The company deals more with high-growth equity funds and retirement plans, designed for long-term wealth accumulation.

- Axis Mutual Fund: Axis Mutual Fund mainly deals with innovative schemes that have a rational distribution of risk and returns to attract a wide range of investors.

- Aditya Birla Sun Life Mutual Fund: It is famous for ELSS or equity-linked saving schemes. The scheme enables a tax-saving investment.

Development Banks in India

Development banks provide long-term finance and project-specific loans which help to raise finance for special sectors like agriculture, rural development, and small-scale enterprises. Underdeveloped regions of India are promoted by Development banks through priority sectors. Some of the Examples of Development Banks are:-

- NABARD: National Bank for Agriculture and Rural Development. It finances agricultural and irrigation projects that address rural development issues. It provides micro-credits to farmers.

- SIDBI: Small Industries Development Bank of India. It creates small and medium enterprises through loan, equity, and capacity building.

- EXIM Bank: It arranges export credit as well as project finance for overseas investments by Indian enterprises.

- ICICI Bank (as Development Bank): The bank was in fact a development bank, that is, a bank that provides funds for infrastructural and industrial projects before transforming into a commercial bank.

- IDBI Bank (Industrial Development Bank of India): IDBI was formed as a development bank that finances industrial growth and infrastructure projects. Why these institutions matter

Why Financial Institutions Matter?

Financial institutions are the backbone of the Indian economy through basic services.

- Economic Growth: They finance industrial and infrastructure projects which contributes to the GDP’s growth.

- Financial Inclusion: NBFCs and microfinance institutions offer banking services to the rural and the underbanked.

- Risk Aversion: Insurance companies and mutual funds avoid financial risks that may lead to instability.

- Capital Building: Development banks and mutual funds help in savings and investment, thereby building a robust financial system.

Financial institutions FAQs

What is a financial institution?

A financial institution is an organization that provides financial services like deposits, loans, and investments. Banks, insurance companies, and NBFCs are examples of financial institutions.

What are the types of financial institutions?

The types of financial institutions include banking financial institutions like commercial banks and non-banking financial institutions like NBFCs. Other types include insurance companies and mutual funds.

What are examples of non-banking financial institutions?

Examples of non-banking financial institutions include Bajaj Finance, LIC Housing Finance, and Muthoot Finance. These entities provide loans, investments, and credit facilities but cannot accept public deposits.

Are financial institutions’ examples safe?

Financial institutions vary in safety. Regulated entities like public banks are safer, while unregulated institutions carry higher risks. Always choose institutions with proper oversight.

Why are financial institutions important?

Financial institutions, therefore, promote economic growth through the provision of funds, managing risks, ensuring financial stability, and efficient capital allocation. Besides, they ensure financial inclusion and innovation.