Receivable and payable management is managing a business’s inflow and outflow of payments intelligently. It ensures excellent cash flow in an organization and efforts to minimize financial risks. It also bridges the gap between a business with its customers and suppliers. The sophisticated receivable and payable management system suffices to maintain the records of payments due to the organization for averting any cash crunch or late payment penalty. Effective management improves businesses’ financial health, decision-making ability, and reputation, besides budget planning and working capital improvement.

Without proper receivable and payable management, businesses face economic instability, strained relations with suppliers, and in the end, loss of revenue.

Receivable and Payable Management Meaning

The receivable and payable management process involves looking into the amounts a company owes to others and the amount it is undoubtedly due to receive. This makes money flow smoothly and seamlessly and ensures the required financial standing is observed. Receivables are just amounts a business expects from its customers, while payables are those owed to suppliers or creditors.

A business must collect money from customers promptly, and a paucity of cash will arise. Equally, a company must discharge its obligations to payables to avoid damage to its reputation among suppliers. A good balance between receivables and payables must exist for a business to run smoothly. A company monitors due dates, automates invoices, and sets credit policies to reduce payment delays.

Objectives of Receivable and Payable Management

Without such an appropriate system, businesses will continue to suffer from payment delays and incur mounting debts, resulting in loss of business continuity. The key features of receivable and payable management assist in maintaining a healthy cash flow in a business environment. Following are five essential features elaborated upon.

Cash Flow Optimization

A well-functioning receivable and payable management system ensures necessary cash flow. Companies are to monitor incoming and outgoing payments efficiently. Cash flow optimization ensures that companies have secure finances and are not in a liquidity crisis. When a business collects payments from its customers promptly, it has enough money to pay for its operations.

Credit Management

Management of credit policies is a necessity for good financial health. Companies should have defined credit terms for customers and suppliers. Credit should be limited enough to not allow for excessively high outstanding balances. Before granting credit, a business should conduct an assessment of the creditworthiness of customers. This reduces bad debts caused by non-payment and guarantees appropriate payment periods. With the invoicing automation in place, bills would invariably get sent over as and when they are due.

Analysis and Financial Reporting

With regular financial analysis, businesses can keep track of their receivables and payables. Reports give insight into the trends of payments, the outstanding balances, and the cash flow projections.

Such analysis of the financials would help better decision-making and highlight possible financial risks so that companies can change their credit policies accordingly.

Supplier and Customer Relationship Management

Good or strong relationships with suppliers and customers ensure the smooth undertaking of operations. A timely payment builds trust and proves beneficial in further business negotiation terms. Open dialogue allows for the negotiation of favorable payment terms. Late payments can ruin relationships and disrupt businesses. A sound receivable push-and-pull system would de-escalate frictions along the way and ensure all-round, extended partnerships.

Working Capital Management

Managing these activities ensures financial viability and operational fluidity on the business’s part. It represents a study of all cash-related decisions in a company, including cash, cash equivalents, receivables, stock, payables, and short-term loans. Working capital management considers the trade-off between maximizing company profitability through capital investments and the financial stability of the yearly income, costs, and/or cash flow from the security rank to be liquidated. Working capital management is handling any asset or liability by working with its respective cash account.

Features of Receivable and Payable Management

Functions of the working capital may include managing cash flow and cash surplus in open market operations through which short-term money is given on loan to others; controlling trade receivables; financing inventories and purchase and factoring; managing cash for making timely payments; ensuring proper calculation of payment periods; and issuing postdated checks.

Timely collections of cash

One of the main goals of receivable administration is to ensure the payment is received in time. Late collections may aggravate the situation with bad debts. Hence, the business must have clear credit policies to stimulate early payment behavior.

Minimizing Financial Risks

The creation of accounts receivable and accounts payable management minimizes financial risks. Delayed customer payments mount the risk of growing bad debts; however, delayed payments to suppliers reduce business credibility.

A well-organized system reduces credit risks and ensures smooth running. Businesses should assess customers’ creditworthiness before establishing a credit relationship, which would diminish payment defaults.

Enhance Operational Efficiency

Optimized receivable and payable management increases efficiency within an enterprise. Businesses can know their financial track with automation, invoice tracking, and financial analysis.

Streamlined financial processes reduce human errors and unnecessary manual labor and enhance accuracy.

Strong Business Relations

Late payments create havoc and act as a stumbling block for businesses. On the other hand, established supplier relationships lead to favorable credit terms and sometimes discounts, while amicable relationships with customers usher business growth.

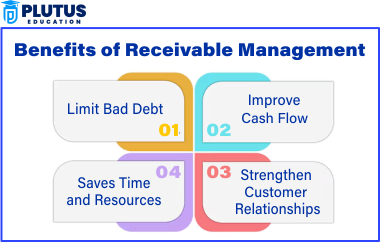

Benefits of Receivable and Payable Management

Receivables and payables management confer countless advantages to working business processes. Effectively controlling these activities leads to better cash flow management, reduced financial risk, and strained relationships. Below are the highlights of the preliminaries and the most important benefits.

Improved Cash Flow Management

Regular cash inflow and cash outflow are equally vital for the day-to-day operation of running a business concern. Receivables and payables management ensures that cash inflows and outflows happen at the right time. The company can plan its expenses well and promptly avert crises regarding liquidity. With proper cash flow management, the company adds stability to its financial future and supports its growth.

Reduced Bad Debts and Payment Defaults

The efficiency of receivable management minimizes the chances of bad debts. Credit should be offered to customers only after assessment of their creditworthiness. Follow-up and reminders help produce payment default scenarios.

Enhanced Financial Planning and Decision Making

Financial planning is easy with good receivable and payable management. The companies can forecast revenues, plan their expenses, and allocate funds. From pattern recognition during financial analysis, firms can feed their strategic decisions. An orderly payment system would keep the firms financially healthy and viable.

Improved Supplier and Customer Relations

Paying suppliers punctually means more favorable terms and discounts for businesses. Strong partnerships with suppliers open more avenues for business. Customers favor businesses that show fair, reasonable, open, and transparent credit policy practices. Prompt invoicing and collection will go a long way in fostering customer satisfaction and loyalty.

Improved Profitability and Growth of a Business

Robust credit management earns businesses money in the form of cost savings. Lower financial risks, stronger cash flow management, and timely payment collection correlate with higher profit margins. Following statutory financial management, the business can invest its remaining finances into growth opportunities.

Relevance to ACCA Syllabus

Accounts Receivable and Payable management is a significant issue revolving in the ACCA Financial Management syllabus. Professionals will gain insight into increasing liquidity and profitability through knowledge of working capital management, with special emphasis on receivables and payables optimization. Financial managers must ensure sustenance through effective credit control, cash flow forecasting, and supplier negotiations.

Receivable and Payable Management ACCA Questions

- What is the primary objective of accounts receivable management?

A) Maximizing sales revenue at all costs

B) Minimizing the cost of bad debts while maintaining sales levels

C) Extending the credit period indefinitely

D) Avoiding credit sales altogether

Ans: B) Minimizing the cost of bad debts while maintaining sales levels

- Which of the following strategies helps reduce the risk of bad debts?

A) Offering longer credit terms to all customers

B) Implementing a strict credit approval process

C) Increasing accounts receivable balances

D) Reducing inventory levels

Ans: B) Implementing a strict credit approval process

- What is the purpose of an aging schedule in receivables management?

A) To forecast future sales revenue

B) To track overdue accounts and assess collection efforts

C) To determine the value of non-current assets

D) To analyze supplier payment trends

Ans: B) To track overdue accounts and assess collection efforts

- Which of the following would most likely improve cash flow in a business?

A) Extending payment terms with customers

B) Reducing the credit period given to customers

C) Increasing inventory levels

D) Paying suppliers immediately

Ans: B) Reducing the credit period given to customers

- A company negotiates longer payment terms with suppliers while maintaining its receivable collection period. What impact does this have?

A) Increases working capital investment

B) Reduces cash flow efficiency

C) Improves cash flow

D) Increases financial risk

Ans: C) Improves cash flow

Relevance to US CMA Syllabus

The US CMA syllabus covers working capital management extensively, as it is essential for financial planning and decision-making. Managing receivables and payables optimizes cash flow, reduces financial risk, and enhances profitability. Understanding discount policies, credit risk analysis, and supplier negotiations is crucial for CMAs.

Receivable and Payable Management US CMA Questions

- What is the effect of a liberal credit policy on accounts receivable?

A) Increases sales but may lead to higher bad debts

B) Reduces sales and minimizes bad debts

C) Improves immediate cash inflows

D) Decreases the accounts receivable turnover ratio

Ans: A) Increases sales but may lead to higher bad debts

- Which financial metric helps measure the efficiency of receivable management?

A) Days Payable Outstanding (DPO)

B) Days Sales Outstanding (DSO)

C) Inventory Turnover

D) Gross Profit Margin

Ans: B) Days Sales Outstanding (DSO)

- A company is considering offering a cash discount to customers. What is the primary benefit?

A) Increases cash inflows and reduces the collection period

B) Reduces total revenue and profitability

C) Increases accounts payable balances

D) Delays payment to suppliers

Ans: A) Increases cash inflows and reduces the collection period

- What is the impact of reducing the cash conversion cycle?

A) Improves liquidity and reduces the need for external financing

B) Increases the cost of goods sold

C) Increases working capital requirements

D) Extends the credit period for customers

Ans: A) Improves liquidity and reduces the need for external financing

- Which of the following best describes the working capital financing strategy where long-term assets are financed by long-term sources, and current assets by short-term sources?

A) Aggressive strategy

B) Conservative strategy

C) Moderate strategy

D) Risk-free strategy

Ans: C) Moderate strategy

Relevance to US CPA Syllabus

Receivable and payable management is covered under the CPA’S financial accounting and reporting (FAR) and business environment and concepts (BEC) sections of the US CPA syllabus. Proper handling of receivables and payables ensures compliance with accounting standards and optimizes working capital, impacting financial health and liquidity.

Receivable and Payable Management US CPA Questions

- Which accounting standard governs the recognition of trade receivables?

A) ASC 606

B) ASC 310

C) ASC 842

D) ASC 740

Ans: B) ASC 310

- What happens when a company writes off an account receivable as uncollectible under the allowance method?

A) Increases net income

B) Reduces net income

C) Has no impact on net income

D) Increases total liabilities

Ans: C) Has no impact on net income

- Which ratio measures how efficiently a company collects receivables?

A) Accounts Payable Turnover

B) Quick Ratio

C) Receivables Turnover Ratio

D) Current Ratio

Ans: C) Receivables Turnover Ratio

- A company delays payments to suppliers beyond the agreed terms. What is a potential consequence?

A) Improved cash flow without consequences

B) Strengthened supplier relationships

C) Potential loss of trade discounts and damaged credit reputation

D) Reduction in accounts receivable balance

Ans: C) Potential loss of trade discounts and damaged credit reputation

- How are accounts payable classified in financial statements?

A) Current liabilities

B) Current assets

C) Non-current liabilities

D) Equity

Ans: A) Current liabilities

Relevance to CFA Syllabus

Receivable and payable management is relevant to the CFA syllabus under corporate finance and financial reporting analysis. Understanding these concepts helps assess liquidity, manage financial risk, and analyze a company’s working capital efficiency to make informed investment and financial decisions.

Receivable and Payable Management CFA Questions

- What does an increasing accounts receivable turnover ratio indicate?

A) Slower collection of receivables

B) Faster collection of receivables

C) Higher bad debts

D) Increased inventory levels

Ans: B) Faster collection of receivables

- A firm with a high days payable outstanding (DPO) may indicate:

A) Strong supplier relationships and optimal cash flow management

B) Poor liquidity and potential supplier disputes

C) Immediate payments to suppliers

D) Increased bad debt expenses

Ans: B) Poor liquidity and potential supplier disputes

- What is the primary trade-off in receivable management?

A) Sales growth vs. credit risk

B) Inventory turnover vs. net income

C) Equity financing vs. debt financing

D) Dividend policy vs. capital gains

Ans: A) Sales growth vs. credit risk

- Which working capital ratio measures the number of days taken to convert working capital into cash?

A) Current Ratio

B) Quick Ratio

C) Cash Conversion Cycle

D) Interest Coverage Ratio

Ans: C) Cash Conversion Cycle

- If a company wants to improve its liquidity position, which of the following strategies would be most effective?

A) Reducing credit sales and improving collections

B) Increasing credit period for customers

C) Reducing payables deferrals

D) Holding more inventory

Ans: A) Reducing credit sales and improving collections