The Sahara scam is one of the major financial scams in India which takes advantage of regulatory loopholes. And millions of retail investors are the targets of such scams. In the case of Sahara Group, driven by Subrata Roy, the group has confessed to illegally raising money through fake financial schemes. Between 2008 and 2011, Sahara Group raised more than Rs 24,000 crore, that is, $3 billion, with the help of the tool. Through unregistered financing known as Fully Convertible Debentures (OFCD), the company attracts this money from more than 30 million retail investors, most of whom reside in Rural and semi-urban areas and have stable returns for their Promising investment.

The case has been on for more than a decade. Thus, millions of investors cannot be aided in their time of need. The law requires that money be returned, yet nothing happens. The scandal draws attention to weaknesses in India’s regulatory structure and the challenges in safeguarding small investors in a huge and heterogeneous economy.

Why is the Sahara Scam in News?

Sahara scams regularly make headlines. Because the scam still hasn’t been resolved. The court proceedings are still ongoing. And the suffering of investors facing fraud. So, even nearly two decades after the scandal, Sahara Group founder Subrata Roy is always under the scrutiny of legal books and public reaction.

In July 2023, the Indian government received news about a project in which Sahara Group plans to return this amount to investors by depositing Rs 5,000 crore with the Securities and Exchange Board of India. Another reason why the scandal made headlines was the extension of Subrata Roy’s imprisonment for failing to comply with a court order. And spent time in court custody.

The case has become a symbol of how poor corporate governance and lax regulatory oversight can result in widespread financial harm. The ongoing legal battle and slow settlement process keep the issue relevant and in the public discourse.

What Was the Scam All About?

The Sahara scam involved the illegal raising of funds by the Sahara Group through two companies: the Sahara India Real Estate Corporation Limited and the Sahara Housing Investment Corporation Limited. Important Ingredients of the Scam

- Issue of Illegal Financial Securities: The Sahara Group mobilized ₹24,000 crore through OFCDs, which are financial instruments through which the investor is given an option to convert his debentures into equity shares at a later date. OFCDs need regulatory approval, which was not taken by Sahara.

- Misrepresentation of Facts: Sahara claimed that OFCDs belonged to a private placement, which implies it was available to a selected few. Instead, it reached more than 30 million investors, thus falling under the bracket of a public offering. The SEBI guidelines require extreme regulatory scrutiny of public offerings.

- Diversion of Funds: The money raised was instead put into businesses that were not legitimate, such as real estate, hospitality, and media ventures.

- Lack of Investor Records: Sahara did not keep proper records of its investors; hence it became impossible to cross-check the repayment claims and affected people.

- Willful ignorance of rules: The company ignored several notices and advisories issued by SEBI, which further delayed the investigation and settlement process.

This makes one of the biggest financial frauds in India, the quantum of scams but also simply because the rules are being violated.

How Did the Case Proceed?

SEBI launched an investigation into the company’s money-making activities in the Sahara scam in 2011. The case soon turned into a long-running courtroom drama. Cases appointing various agencies legal movement Lots of twists and turns. The timeline of events is as follows:-

Basic Knowledge About Surveying

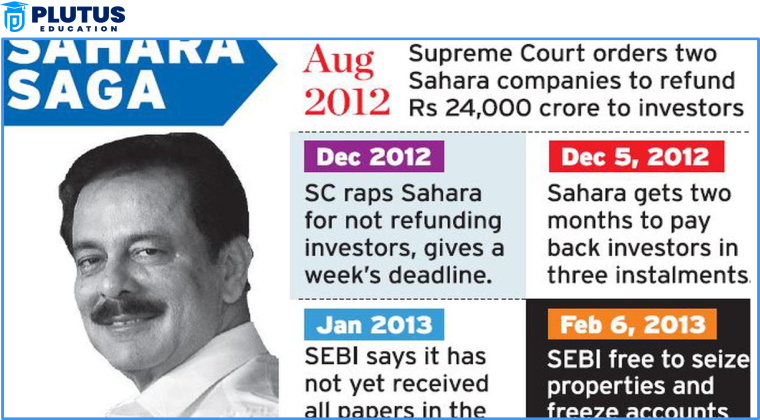

In 2011, SEBI found that Ciracl and SICL had collected OFCD worth Rs 24,000 crore without proper distribution. SEBI declared the collection illegal and asked the company to return the collected money to investors.

Judicial Interventions by the Supreme Court

In August 2012, the Supreme Court of India confirmed the SEBI decision and ordered Sahara to return all the money with a 15% annual interest. The court ordered that the money should be deposited with SEBI, which would track the refund process.

Subrata Roy Arrested

On his part, when Sahara failed to comply with the Supreme Court order, Subrata Roy was detained for contempt of court in March 2014 based on this. He was held in judicial custody before being released on bail in 2016 for nearly two years after…

A lawsuit is Currently Being Filed

Sahara claims that the bulk of the funds were returned directly to investors and receipts were issued. However, SEBI disputes this and contends that the receipts are not verifiable or incomplete. According to this argument, A refund has been given. It stalled and investors were left in limbo.

Government Refund Scheme

The government intervened by announcing that by 2023, Sub-Saharan Africa would return investors using Sebi’s Rs 5,000 million. This amount is just the tip of the iceberg. Of all things, only refunds are slow because identity verification is a challenge.

Where Are the Investors?

This has left millions of investors in a financial mess and confusion. Most of the investors are from rural and semi-urban areas where formal banking services are not available. The Sahara scam targeted small savers, luring them into attractive returns while portraying the company as a trustworthy and safe investment option. All these people, who had risked their lifetime savings with Sahara Group, are now getting the bitter taste of betrayal as the scam unwinds. Most investors are low-income farmers, laborers, and small business owners. They have been attracted to the schemes through aggressive marketing and perceived security in their brand. Financial education has been deprived of them. Investors’ Problems are discussed below:-

1. Reimbursement is Delayed

The refund process has been agonizingly slow and most people have yet to collect their returns from the hard-earned money. As much as SEBI tried returning the amount collected by Sahara for the affected investors, it managed to return just a small percent of the entire amount collected from the people by Sahara. Financial misery to such victims adds a lot more for those who earn their living in day-to-day survival by relying on their savings.

2. Lack of Awareness

Most of Sahara’s investors are not aware of their rights or the refund process. Generally, this is true in most remote and rural setups with low levels of exposure to news and financial literacy. Therefore, many investors remain in the dark about the ongoing legal processes in place to acquire their money.

3. Problems in Verifying Identity

The reimbursement procedure requires that investors provide cogent evidence of their investments such as bond certificates and receipts. However, Sahara kept no records. Most of the investors have not documented their copies, and many have lost them, causing the verification process to be more cumbersome and problematic in the long run. SEBI and the government cannot verify investor claims, which has caused very huge delays.

4. Erosion of Trust

The Sahara scam has resulted in a general erosion of trust in non-banking financial institutions (NBFCs). Investors in rural areas have become very reluctant to invest in similar schemes fearing that they would again lose their savings. This erosion of trust has, in turn, created a ripple effect on the larger financial system because it has kept small savers away from genuine financial products.

Government Measures to Resolve Investor Complaints

In July 2023, the Indian government took a very proactive step in handling the grievances of Sahara investors. It announced that it would refund ₹5,000 crore already deposited by the Sahara Group with SEBI. The government has facilitated the process by making an online portal and has invited all the investors to submit claims.

Features of the Refund Scheme

- Eligibility Criteria: The investors had to provide proof of the investments in the form of bond certificates or receipts issued by the firm.

- Verification Process: All claims were verified by SEBI and the government, and their genuineness was confirmed.

- Refund Distribution: All claims that had been verified were made into refunds for them.

Despite all these efforts, the scheme has been facing various challenges. The number of claims received is too huge, and the amount of funds available is much lower than the total amount owed to the investors. Also, the verification process has been very slow because of incomplete documentation and technical problems in the online portal.

This move from the government is right in terms of making things happen and will still, at least not suffice the gigantic extent of this issue. Under the scheme, stronger mechanisms were seen to better protect the small investor while quick refund procedures were addressed.

What’s the Road Forward?

Only a combination of regulatory reform, government action, and public investor education will successfully prevent another such debacle in the future and unravel the Sahara scam.

While making amends for wronged investors should be one part of any effort, rectifying the structural deficiencies that let the Sahara scam succeed must be a critical focus area.

Toughening up on Compliance

- Ensuring better compliance: Regulators like SEBI need to enforce tight compliance measures at the company level also to raise funds from the public. Scrutiny must be carried out on all the financial instruments raised as public and private. Companies that fail to comply with norms must be subjected to severe penalties immediately.

- Real-time Monitoring: Regulators can use advanced technology to monitor financial transactions in real time, which helps them detect fraud at an early stage. Advanced artificial intelligence and data analytics could be crucial tools in identifying suspicious patterns and avoiding scams before they get out of hand.

- Transparency in Fundraising There needs to be very detailed and transparent records of the investors and all the funds raised. The books must be opened for the accessing of the same by the relevant regulatory bodies. In this eventuality, if a fraud has occurred, they can readily respond.

Fast Refunds

- Rapid Verification System: The government along with SEBI must concentrate on technology-based systems that will allow for fast verification. Blockchain is one of the technologies that can help develop an unalterable and transparent verification system of claims of investors.

- Increased Interference from Government: More funds must be sanctioned by the government to cover the deficit of Sahara’s SEBI deposits so that more investors get their refund immediately and out of their financial distress.

- Awareness Campaigns: There is a need to create awareness among investors about the refund scheme and the risks of unregulated investments. The government must organize campaigns in regional languages so that rural and semi-urban people can also be targeted.

Lessons from the Sahara Scam

The Sahara scam opens one’s eyes to the world of financial literacy and due diligence. Investors should always check whether the investment scheme is valid or not before putting their funds in it. Also, the companies in which they are investing must adhere to regulatory requirements and be transparent about their operations.

Role of Policymakers

Therefore, policymakers have to focus on bringing in a sound protection framework for small investors. The existing rules have to be more stringent against fraudulent companies, and mechanisms for grievance redressal by investors should improve. Restoring the confidence of the public in the financial system calls for the active involvement of all stakeholders.

Sahara Scam FAQs

1. What is Sahara Scam?

Two Sahara companies fraudulently raised Rs 24,000 crore by collecting unregistered bonds from more than 100,000 investors.

2. Why has the sub-Saharan scam been exposed recently?

Under the government’s draft plan for 2023, investors will get their money back through Sahara deposits with SEBI, and several court cases mean the scam isn’t going to calm down in court any time soon.

3. How do the investors get back their money?

There is a website by the government where refund requests can be placed. Evidence of investment and some form of identification will be needed.

4. What is the Role of SEBI in the fraud?

SEBI conducted an inquiry. Declared that the mode of raising the amount by Sahara was illegal. Sebi proceeded with legal remedies recovered the money from the respondents and issued cheques.

5. Effects of deception in Sub-Saharan Africa

Millions of retail investors are impacted. And public confidence in financial institutions has eroded. The regulatory framework is riddled with gaping holes.