The term what is a transaction is fundamental to understanding how money, goods, or services are exchanged between individuals, businesses, or organisations. A transaction refers to any exchange of value. Where one party gives money or a product or something of value and receives it. In return, Transactions occur daily in personal life, business, and the global economy. These transactions support all economic activities.

What is a transaction in accounting? Recording and documenting such exchanges in a structured manner to monitor financial status is a transaction. Transactions are financial measures that affect the financial position of the person or entity involved.

For example, when a business purchases raw materials, it records this event as a purchase transaction. In the same way, When a person pays rent, It is considered a personal financial transaction. The study of behaviour covers more than essential exchanges. This includes understanding classifications. Accounting methods and the impact on financial reporting

What is Transaction?

A transaction is a transfer of value between two parties. It could be an exchange or an agreement where one thing is given and another received in return. It could be in the form of cash, goods, services, or any other resource. In monetary terms, it is seen when a person pays for groceries. It is also seen when goods are exchanged. Business-wise, A business transaction refers to any activity that directly impacts the company’s financial records. This may be selling products to customers. Payment of employees or buying office equipment In accounting, transactions are an important component of financial management.

All economic and financial activities can be made of transactions. These transactions are divided into different categories based on the purpose, nature, time of occurrence, and their effect on the books of accounts. It helps an individual or an enterprise in arranging the economic activities effectively and in keeping accurate accounts. The different classifications of transactions are explained as follows.

Characteristics of Transaction

Some of the features include:

- Involvement of both parties: Every transaction involves at least two parties, such as a buyer or seller. Loans and Borrowers Transfer of Value There must be a transfer of value, which may be in the form of money, goods, or services.

- Financial Measurement: A transaction must be measured in monetary terms to qualify as an accounting transaction.

- Impact on financial records: Transactions affect the financial position of the individuals involved. Changes in assets, liabilities, or equity.Understanding which behaviours help us understand how these events affect business and personal finances.

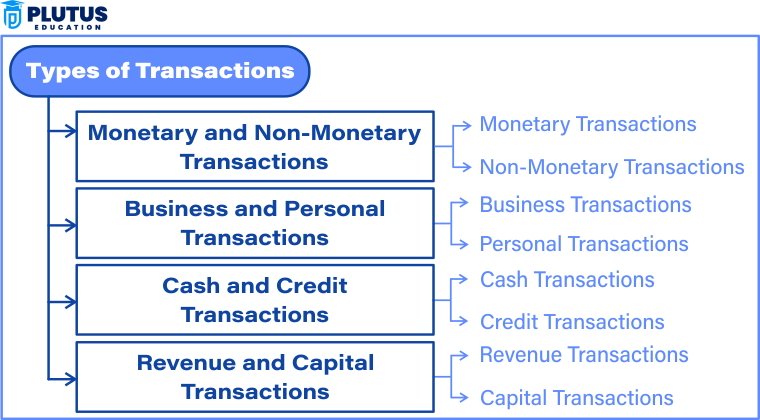

Types of Transactions

Transactions are the building blocks of all economic and financial activities and can be categorised into several types. These categorisations are based on their purpose, nature, timing, and the effect they have on financial records. Understanding the different types of transactions can help individuals and businesses better organise their economic activities and maintain clear records. We discuss the classifications of transactions in detail below.

- Monetary and Non-Monetary Transactions

Monetary and non-monetary transactions differ in the involvement of money. Monetary transactions use cash or digital payments, while non-monetary transactions involve the exchange of goods or services without money.

Monetary Transactions: Money is the medium of exchange in monetary transactions. Such transactions are easy and occur when cash, debit cards, credit cards, or any other financial instrument is used to make a payment. Monetary transactions form the bulk of modern economies since they quickly transfer value.

Monetary Transactions: For example,

- Buying groceries at a grocery store with cash or a debit card.

- Digital wallet and net banking, payment for the services done online.

- Pay rent by the month with a bank transfer.

- Individuals and enterprises require money, and any money transaction can affect the cash flow. That’s a critical component in the financial planning and management process.

Non-Money Transactions: Non-Money Transactions: Non-monetary transactions do not involve the use of cash or other financial instruments to exchange value; it is exchanged through bartering or swapping goods and services. Although it rarely occurs in the current economy, it still takes place in communities or specific conditions.

Example:

- The farmer who has crops trades them to a carpenter in return for fixing the barn.

- Graphic designer making a company logo in exchange for free accounting services.

- Non-cash transactions should be carried out with much care, especially accounting. Companies must calculate and account for the fair market value of the products or services traded to record the transactions. Such transactions are not cash transactions but are essential in operational and financial records.

- Business and Personal Transactions

Business and personal transactions differ because of their purpose. Business transactions are those that affect the financial situation of a particular business. In contrast, individual transactions refer to non-business activities concerning personal finance, such as daily expenditures or saving.

Business Transactions: A business transaction will be any activity or transaction that will directly affect the account or the company’s financial position.

- Accounting for sales revenues when a client buys a good or service

- Purchasing raw materials or stock inventories to make the products.

- Salaries and utility bills for the employees.

Business transactions are classified into operating, investing, and financing activities in the financial statements.

- Operating Transactions: Sales revenue, rent payments, and utility expenses.

- Investing Transactions: Purchasing machinery or selling the company’s assets.

- Financing Transactions: Money borrowed from banks or issuance of shares for raising capital.

Business transactions are the backbone of financial statements and give insight into the profitability and soundness of a company’s health. Ensuring these transactions are well documented and analysed helps business growth and regulatory compliance.

Personal Transactions: Personal transactions refer to those financial transactions which do not have any relationship with business performance. In general, they only cover a little personal usage and are coupled with normal expenses of daily life, personal investments, or other non-business-related assets.

Example

- Rental of an apartment for personal usage.

- Grocery or clothing purchases for personal use.

- Investment in a fixed deposit for personal savings.

Personal transactions do not directly reflect on the financial position of business. However, they really help in an individual financial planning. The monitoring of personal transactions helps an individual manage his budget well, save efficiently, and plan for future financial goals..

- Cash and Credit Transactions

Cash and credit transactions make up the foundation of financial exchanges. Cash transactions are immediate payment, while credit transactions give room for deferred payments, thus having an impact on cash flow and accounting differently.

Cash Transactions: Cash transactions are one of the direct forms of money exchange. The case happens when one sells an item or product and pays is provided immediately after its sale. One might opt for either a physical cash or electronic debit card.

Examples

- Buying a cup of coffee and then paying for the cup of coffee in cash at that moment. When one pays through a debit card to watch a movie. Direct Cash Deposit into your Savings Account.

- Cash transactions are very fulfilling since there is no deferred payment. They are easy to record, have minimal documentation, and are less complicated than credit transactions. Businesses in small or low-value purchases prefer cash transactions since they are straightforward.

However, cash transactions are also limited. They may be unable to provide essential documents for tax purposes, especially when large amounts of money are involved. Additionally, they do not give one the security of electronic transactions since cash tends to get lost or stolen.

Credit Transactions: Credit transactions are the financial exchanges for payment. The buyer acquires goods or services when the need arises but promises to pay for them afterwards in the case of this kind of transaction. Credit transactions are the basis of modern financial systems since they enable better cash flow management for individuals and businesses.

Example:

- Buying a car on an instalment basis, where the buyer pays monthly instalments instead of the full amount.

- Ordering office supplies on credit from a supplier, with payment due after 30 days.

- Using a credit card to pay for groceries and repaying the credit card bill after the billing cycle ends.

Credit transactions are common business-to-business, or B2B, because they enable businesses to operate without actual cash outlay. For a firm, credit sales affect accounts receivable (the amount due to the company) and accounts payable (the amount the company owes). While credit transactions are convenient, default or delayed payment is always risky. Companies have to carefully consider the creditworthiness of their customers to minimise bad debts. Individuals must also control their credit use to avoid financial strain caused by unpaid bills or high-interest debt.

- Revenue and Capital Transactions

Transactions can be classified based on their impact on a business’s financial position. Revenue and capital transactions are among them.

Revenue Transactions: A business’s activities that increase its income are revenue transactions. These take place very often as part of the company’s daily operations. Revenue transactions are directly reflected in the profit and loss statement, hence reflecting the success of a business in terms of operations.

Examples:

- Selling products to customers.

- Rendering services, such as consulting or repair services.

- Accruing interest on bank deposits.

Revenue transactions directly impact a company’s income and are an essential indicator of its profitability. Businesses must track and analyse these transactions carefully to identify trends, forecast future income, and make strategic decisions.

Capital Transactions: Long-term financial changes of a company result in capital transactions. The record of such transactions will be in a company’s balance sheet. Examples of capital transactions include investing, acquiring, or financing activities. Such transactions are relatively less common than revenue transactions and are usually substantial in amount.

Examples are:

- Purchase of land or machinery for business purposes.

- Issuance of shares to raise equity capital.

- Long-term loan to expand the business.

Capital transactions reflect a firm’s investment policy and its long-term growth prospects. Proper documentation and analysis of such transactions are essential for the organisation’s transparency and satisfying regulatory requirements.

Transactions Under Accrual Accounting

When talking about what a transaction is in accounting, accrual accounting assumes a great place in recording the financial events of a firm. Accrual accounting involves recording the transaction when it takes place rather than the actual cash exchange. This provides an overview of the firm’s financial position and a match of revenues and expenses during the same accounting period.

It is very common to find large businesses and organisations using accrual accounting for proper financial records. For example, if a firm delivers products to a customer in December, but the customer pays the bill in January, then that income is accrued during December under accrual accounting. Likewise, when a business makes electricity consumption during April, but the firm pays the bill during May, that expense accrues during April.

Advantages of Accrual Accounting

Advantages of accrual accounting include:

- Accrual accounting gives a more precise and more accurate picture of financial performance.

- Accrual accounting enables businesses to adhere to accounting standards like GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards).

- It helps organisations manage long-term projects by bringing revenues in the same period as expenses. Accrual accounting, although beneficial, requires careful record-keeping to achieve accuracy and conformity.

Transactions Using Cash Accounting

Cash accounting records a transaction as cash accounting. This accounting system has entries done once the cash has been received or paid. It’s straightforward; however, it is a common practice among smaller businesses and small taxpayers.

For example, cash accounting records the transaction in March if a business renders services in February but receives cash for them in March. If a company pays for office supplies in June, this expense is recorded in June, regardless of when the supplies were delivered.

Advantages of Cash Accounting

Cash accounting has several advantages:

- It is easy to understand and, therefore, easy to implement, making it very suitable for small businesses.

- It provides current information on the cash flow as this helps track the business’s financial position.

- It offers fewer chances for error and less paperwork compared to accrual accounting.

- Cash accounting does not produce a true-to-life picture in the long run because it does not recognise unpaid invoices or accrued expenses.

What is an ACH Transaction?

An ACH transaction is an electronic fund transfer made over the ACH network. This is widely used for direct deposits, bill payments, payroll processing, and online transfers. ACH transactions have become popular lately because they save time and are efficient enough. For instance, when you have a bank deposit of payroll directly into employees’ accounts or when your electricity bill is online, the money is transferred through this ACH mechanism.

Advantages of ACH Transactions

The advantages of making ACH Transactions include:

- They are cheaper for the sender compared to other remittance methods- wire transfers end.

- They reduce the reliance on paper checks, and they are sustainable.

- They are secure and reliable transfers that ensure the safety of the money.

How Do I Void a Pending Transaction?

A pending transaction can be cancelled if one acts in time. Whether an accidental payment or an unauthorised charge, contacting your bank or service provider as soon as possible is essential. Remember to include the sum, date, and transaction number when making a cancellation request. Most banks and other payment services have policies on cancelling transactions; however, not all transactions can be cancelled, mainly once they have been processed. Check the details one more time before confirming payments.

How are Transactions Different in Accounting?

Transactions in accounting are far from regular transactions. Transactions are the recording and documentation of financial activities in a structured manner. Regular transactions such as buying groceries or borrowing money from a friend are usually not recorded formally. In accounting, all the transactions that affect financial records are documented systematically.

For example, if a company sells goods to a customer, its income statement recognises the transaction as revenue. However, if the company buys office equipment, that transaction will be recognised as an asset in its balance sheet. Accounting transactions are significant because they must ensure that a business keeps its accounts properly, prepares the necessary financial statements, and fulfils tax and regulatory requirements.

Transaction in Accounting FAQs

Q1. What is a transaction, in simple words?

The transaction is an exchange of goods, services, or money between two parties. It forms the base of all financial activities and also influences financial records.

Q2. What is a business transaction?

A business transaction can be defined as any financial activity affecting the company’s financial position, such as sales, purchases, or salaries.

Q3. What does recording the transaction in accounting mean?

Recording a transaction in accounting is like recording a transaction in journals or ledgers to monitor income, expenses, and assets.

Q4. What is an ACH transaction?

An ACH transaction refers to the electronic transfer of funds through Automated Clearing.

House network. Everyday ACH transactions include direct deposits and bill payments.

Q5. How do I cancel a transaction?

You can cancel a transaction by contacting your bank or payment service provider, providing transaction details, and following their cancellation policy.